06.19.19

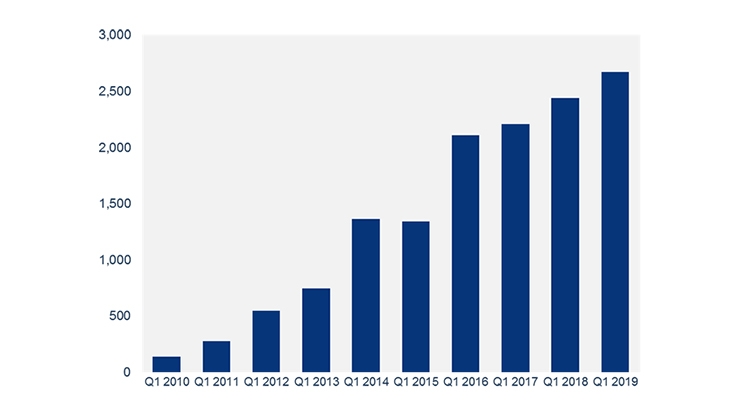

In the first three months of the year, the US installed 2.7 gigawatts of solar photovoltaics (PV), making it the most solar ever installed in the first quarter of a year. With the strong first quarter, Wood Mackenzie Power & Renewables forecasts 25% growth in 2019 compared to 2018, and it expects more than 13 GWdc of installations this year.

This data comes from the new US Solar Market Insight Report from Wood Mackenzie and the Solar Energy Industries Association (SEIA), whom together announced in May that the US hit the two million solar installation milestone during the first quarter of 2019.

“The first quarter data and projections for the rest of the year are promising for the solar industry,” said Abigail Ross Hopper, president and CEO of the Solar Energy Industries Association. “However, if we are to make the kind of progress we need to make the 2020s The Solar Decade, we will need to make substantial policy and market advances.”

The largest share of installations during the record-breaking quarter came from the utility PV segment, with 1.6 gigawatts coming on-line, making up 61% of PV capacity installed. The report notes that with 4.7 gigawatts of large scale projects under construction, 2019 is on track to be a strong year for utility PV, with 46% growth over 2018 expected.

“Voluntary procurement of utility PV based on its economic competitiveness continues to be the primary driver of projects announced in 2019,” said Colin Smith, Wood Mackenzie senior solar analyst. “While many states, utilities and cities have announced or proposed 50% or 100% renewable energy or zero-carbon standards, the announcements have not yet resulted in an uptick in RPS-driven procurement."

The residential market experienced annual growth as well.

According to the report, the US saw 603 megawatts of residential solar installations during the first quarter, up 6% annually.

“Despite steady installations in Q1 2019, the residential market is still highly reliant on legacy state markets, such as California and the Northeast, which have seen only modest to flat growth over the past several quarters,” said Austin Perea, Wood Mackenzie solar analyst. “As these major state markets continue to grow past early-adopter consumers, higher costs of customer acquisition will challenge the industry to innovate product offerings and diversify geographically.”

In fact, the report notes that 29% of residential capacity in Q1 2019 came from markets outside the top 10 solar states by capacity, the highest share for emerging markets in industry history.

The non-residential segment, which represents commercial, industrial and public sector distributed solar, saw 438 megawatts of PV installed on the quarter, which was down on both a quarterly and annual basis. According to the report, this is largely a result of state-level policy reforms in historically strong markets for the segment including California, Massachusetts and Minnesota. The authors point to new community solar mandates in New York, Maryland, Illinois and New Jersey that will help reinvigorate the segment beginning in 2020.

Total installed US PV capacity will more than double over the next five years, with annual installations reaching 16.4 GWdc in 2021 prior to the expiration of the residential federal Investment Tax Credit (ITC) and a drop in the commercial tax credit to 10% for projects not yet under construction.

Caption: US PV capacity installed in the first quarter, Q1 2010 – Q1 2019 (MWdc). Source: Wood Mackenzie / SEIA US Solar Market Insight Report, Q2 2019

This data comes from the new US Solar Market Insight Report from Wood Mackenzie and the Solar Energy Industries Association (SEIA), whom together announced in May that the US hit the two million solar installation milestone during the first quarter of 2019.

“The first quarter data and projections for the rest of the year are promising for the solar industry,” said Abigail Ross Hopper, president and CEO of the Solar Energy Industries Association. “However, if we are to make the kind of progress we need to make the 2020s The Solar Decade, we will need to make substantial policy and market advances.”

The largest share of installations during the record-breaking quarter came from the utility PV segment, with 1.6 gigawatts coming on-line, making up 61% of PV capacity installed. The report notes that with 4.7 gigawatts of large scale projects under construction, 2019 is on track to be a strong year for utility PV, with 46% growth over 2018 expected.

“Voluntary procurement of utility PV based on its economic competitiveness continues to be the primary driver of projects announced in 2019,” said Colin Smith, Wood Mackenzie senior solar analyst. “While many states, utilities and cities have announced or proposed 50% or 100% renewable energy or zero-carbon standards, the announcements have not yet resulted in an uptick in RPS-driven procurement."

The residential market experienced annual growth as well.

According to the report, the US saw 603 megawatts of residential solar installations during the first quarter, up 6% annually.

“Despite steady installations in Q1 2019, the residential market is still highly reliant on legacy state markets, such as California and the Northeast, which have seen only modest to flat growth over the past several quarters,” said Austin Perea, Wood Mackenzie solar analyst. “As these major state markets continue to grow past early-adopter consumers, higher costs of customer acquisition will challenge the industry to innovate product offerings and diversify geographically.”

In fact, the report notes that 29% of residential capacity in Q1 2019 came from markets outside the top 10 solar states by capacity, the highest share for emerging markets in industry history.

The non-residential segment, which represents commercial, industrial and public sector distributed solar, saw 438 megawatts of PV installed on the quarter, which was down on both a quarterly and annual basis. According to the report, this is largely a result of state-level policy reforms in historically strong markets for the segment including California, Massachusetts and Minnesota. The authors point to new community solar mandates in New York, Maryland, Illinois and New Jersey that will help reinvigorate the segment beginning in 2020.

Total installed US PV capacity will more than double over the next five years, with annual installations reaching 16.4 GWdc in 2021 prior to the expiration of the residential federal Investment Tax Credit (ITC) and a drop in the commercial tax credit to 10% for projects not yet under construction.

Caption: US PV capacity installed in the first quarter, Q1 2010 – Q1 2019 (MWdc). Source: Wood Mackenzie / SEIA US Solar Market Insight Report, Q2 2019